Decent Africa announces the appointment of Hon. Joyce Nabbosa Ssebugwawo, Minister of State for Information Communication Technology, as the new patron of the organization. This partnership signifies a significant step towards fostering a culture of decency and respect across the African continent.

Hon. Ssebugwawo brings a wealth of leadership experience, community engagement, and a steadfast commitment to decency and public service, making her an invaluable addition to Decent Africa. Her illustrious career in community mobilization, ICT, and visionary leadership will play a pivotal role in advancing initiatives that promote integrity, elegance, and impactful leadership among Africa’s prominent figures.

In her capacity as Patron, Hon. Ssebugwawo will play a crucial role in shaping the strategic direction of Decent Africa and expanding its outreach. Her expertise in decency and digital technologies perfectly aligns with the organization’s objectives to utilize digital media for broader societal impact and empower future generations through innovative educational and advocacy programs.

Decent Africa is confident that Hon. Ssebugwawo’s guidance will enhance its initiatives and extend its impact deeper into the community. The organization eagerly anticipates productive leadership and collaboration with Hon. Ssebugwawo as they continue to champion and uphold the values of decency and decorum across Africa.

In the March 2024 issue of Digital Money Movers, we present profiles of 40 women leaders from diverse African regions. We aim to provide an overview of the existing challenges, barriers, opportunities, and exemplars critical to fostering an inclusive innovation curve that can benefit all members of society.

Our publication highlights the importance of recognising individuals leading the way and addressing the challenges faced by African women leaders, who can serve as models for others seeking to advance their careers in innovation and entrepreneurship.

By highlighting the experiences of these women, we hope to inspire new ideas and collaborations that can contribute to sustainable economic growth and social progress in Africa and beyond.

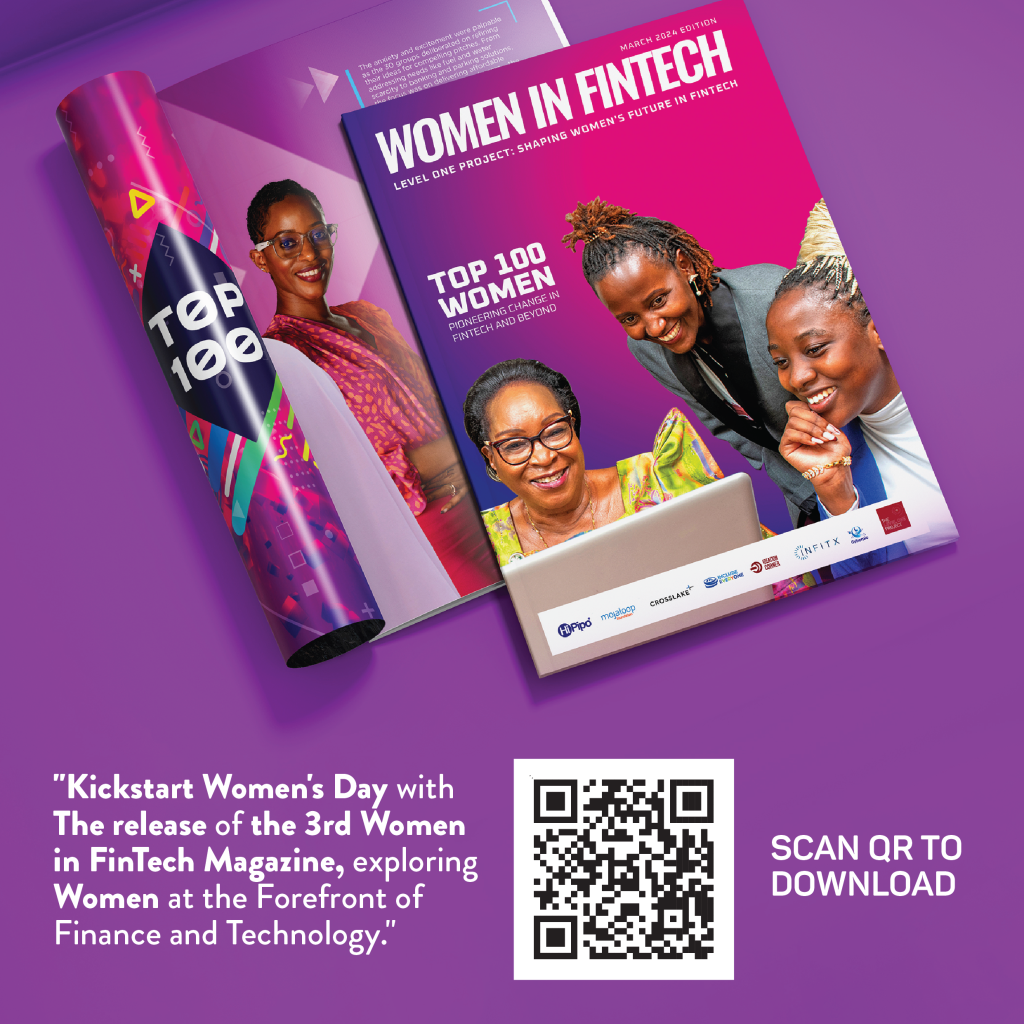

We are thrilled to announce the release of the 2024 HiPipo #WomenInFinTech Magazine on International Women’s Day today.

This edition showcases the stories of women in Uganda and East Africa who have led the way towards financial inclusion, community empowerment, and transformative progress in the FinTech sector.

The publication features a series of inspiring accounts that highlight the pivotal role of women in shaping the landscape of financial technology in Africa.

The February edition of Digital Money Movers, a monthly publication dedicated to exploring the dynamic world of digital innovation and financial services, is now available!

This month’s issue is centred around “Navigating the AI Revolution in Finance and Beyond.”

In the wake of the influential and widely celebrated inaugural “100 Women in FinTech” listing in 2023, we are excited to announce an even more ambitious and impactful edition for 2024. This year’s edition expands on the previous year’s achievements and introduces several new dimensions to recognise and celebrate the women leading the way in the FinTech industry.

In a noteworthy enhancement from last year, the top 100 women selected for 2024 will be honoured with a “Digital Certificate of Excellence.” This prestigious acknowledgement is a testament to their outstanding contributions, service, and societal roles. These are lifelong accolades, empowering recipients to showcase their achievements in their professional biographies and across various social communication platforms.

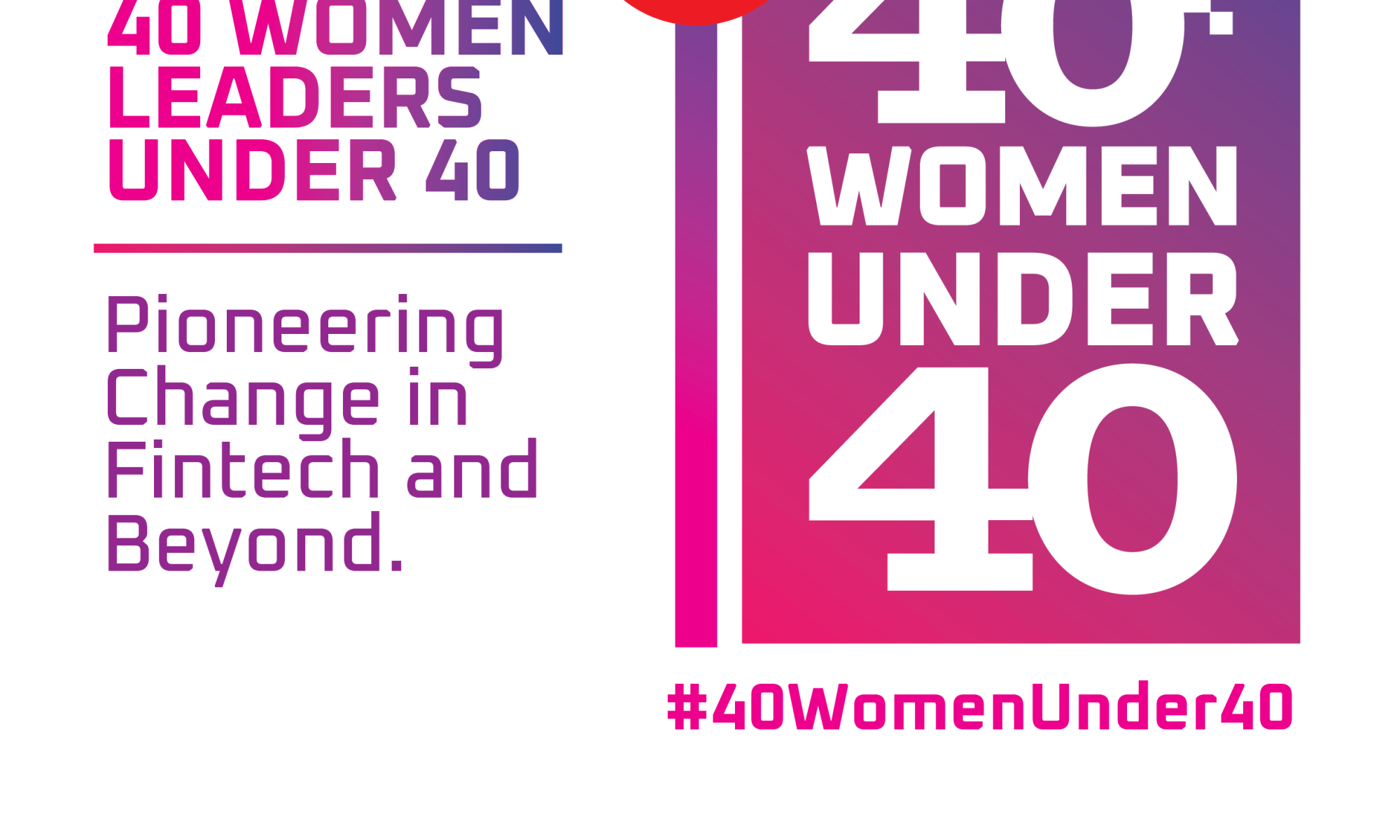

As we approach the International Women’s Day celebrations, we are thrilled to spotlight 40 remarkable women leaders. These leaders are not just making strides in financial inclusion and gender diversity; they are redefining what it means to be a leader in today’s dynamic financial landscape.

Selected through a People’s Choice process, these 40 women represent the very best of innovation, executive leadership, entrepreneurship, and business acumen — all under 40. They are the women who have been directly nominated by those whose lives and careers they have significantly impacted.

Starting January 30th, 2024, we embark on a journey to showcase one exceptional woman leader each day individually. This culminates on March 8th, aligning with International Women’s Day, when the highly anticipated “HiPipo Women in FinTech Magazine” will be published, featuring more inspiring women.

Join us in this celebration as we highlight these trailblazing women excelling in their fields and paving the way for future generations in FinTech and beyond.

Earning money is very hard but spending needs no rocket science. For instance, it is not news that someone can have TSh. 1,000,000 in the morning and by evening, s/he has used up all the money. This may be due to unnecessary spending, extravagance or poor planning.

Nonetheless, Innovators are using technology to develop tools and platforms that can cure such ills. On Day 41 of the 40 Days 40 FinTechs initiative for Tanzania, we interacted with Ronald Mwanyika, the Founder of Pocket Budgeting. Here is the story of how Pocket Budgeting is helping its customers manage their money by spending rightly and setting priorities.

HiPipo: What is Pocket Budgeting?

Ronald Mwanyika: Pocket budgeting is a platform that allows people to master their money and make better financial choices or decisions. What we do is we allow people to spend their money in the right areas or the areas that matter; giving them the ability to better understand how their money comes and how their money goes.

HiPipo: Why should customers be interested in Pocket Budgeting?

Ronald Mwanyika: One of the major reasons why a person should sign up with Pocket is for the person who needs or wants to better master their money and attain that financial freedom, they should sign up with Pocket because it is a platform that will give them tools to better manage their money and also a platform that will give them the knowledge they need to better make their money grow and make their money worth something.

HiPipo: How does one get started on Pocket Budgeting?

Ronald Mwanyika: First and foremost, you must have the application on your phone. And after creating an account, you will be able to add your income. Now, we call it net worth, because according to us, net worth is the money that you have after you have removed all the expenses. So, you add your income, and there are several envelopes, such as spending, there is to pay. That’s an envelope where the people that you have to pay, you also have an envelope of people that have to pay you. And there is an envelope for investing and savings. There is an envelope for expenses. So, once you have added your income, you distribute that money into the respective envelope so that you can know how much money is left. One thing that we believe in is you have to pay yourself first. So, after you remove all the expenses, that net worth that remains is the money that you have that has no use. So, it is like the money that you have paid yourself from the income you have gained. Once you start budgeting your money, you start to see how much money you don’t have, instead of just seeing that, oh, I have this certain amount of money that you don’t know where the money goes.

One of the things that we have tried to address is trying to teach our customers how to best allocate their money. We help them prioritize and make good choices.

HiPipo: What are some of the challenges you have so far faced in this business?

Ronald Mwanyika: One of the major challenges we have so far is the issue that comes with people trusting what you are trying to do because when it comes to money, most people are sensitive about that subject. When I was researching to see if people would be interested in such a platform, most people were saying they were interested, but when it came to transacting money through the platform, it was an issue for them, it was a very sensitive subject.

HiPipo: What are your views about partnerships for start-ups in regards to start-up growth?

Ronald Mwanyika: Partnerships are something that helps the company to grow because a startup has competitors in the market that already know the terrains and most of the things about how the business goes. So, for a startup, partnerships are one thing that helps it to grow and catch up to with who are already in the market. So, I believe also in pocket, as we are growing into the market, we will be able to see the companies that we can best partner with us to be able to fulfil the goals that we set out to fulfil.

HiPipo: What are your views about 40 Days 40 FinTechs?

Ronald Mwanyika: Platforms such as 40 Days 40 FinTechs help FinTechs to best show what they can do. They also help to show the regulators the potential of FinTechs and what they need to thrive. And in a way that if the regulators can best see the values and know how the FinTechs operate, they can then set regulations and rules that best suit the industry, regulations that are pro-start-ups and facilitate FinTech companies.

Include EveryOne Program.

First implemented in Uganda, 40 Days 40 FinTechs is an annual FinTech Innovation initiative presented by HiPipo to recognize and celebrate individuals and organizations who are making significant strides in promoting financial inclusivity through the use of technology.

It is aimed at promoting innovation and collaboration among FinTechs in Africa. The initiative is designed to provide FinTechs and startups with mentorship, training, exposure, and networking opportunities to help them grow and scale their businesses.

40 Days 40 FinTechs initiative Tanzania is part of HiPipo’s broader Include EveryOne Program that is generously supported by the Gates Foundation and implemented in partnership with Level One Project, ICTC Tanzania, Ideation Corner, Cyber PLC Academy, INFITX, Crosslake Technologies, NG Films, Founders Academy and Mojaloop Foundation.

The Include EveryOne program is a beacon of acceleration of FinTech Innovation, empowerment for Women in FinTech and a catalyst for investment and development in the ICT sector. Minus 40 Days 40 FinTechs, other initiatives under the Include EveryOne Program are the FinTech Landscape Exhibition, Women in FinTech Hackathon, Summit and Incubator, Digital Impact Awards Africa and the Digital and Financial Inclusion Summit.

HiPipo is recognized as a premier advocate of digital Innovation and financial inclusion champion, a fervent proponent of the #LevelOneProject. HiPipo has been at the forefront, actively promoting digital innovation, Instant, Inclusive Payment Systems (IIPS), and DFS across Africa. With a legacy of advising, mobilizing, and facilitating the adoption of inclusive financial services, HiPipo’s efforts have been nothing short of transformative! For almost two decades, HiPipo has successfully facilitated the inclusive adoption of these crucial services.

We are pleased to announce the launch of Digital Money Movers, a monthly publication dedicated to exploring the dynamic world of digital innovation and financial services. The journal delves into the compelling stories, significant developments, and influential figures shaping FinTech innovation, digital payments, and financial inclusion across Africa.

Digital Money Movers is designed to be more than a mere publication. It aims to comprehensively explore the key contributors, opportunities and challenges within Africa’s FinTech Innovation, Digital Financial Services (DFS), and Financial Inclusion landscape. Its primary objective is to offer an in-depth view of the trailblazers making a lasting impact in these sectors.

Each month, the publication will shed light on the movers and shakers in this space, highlighting their contributions and the enduring influence they bring. At the end of each year, all insights gathered throughout the months will be compiled into an exclusive edition, offering a holistic view of the advancements and trends witnessed over the months.

In the inaugural edition, we focus on Visa and Mastercard, examining their rivalry and presence in Africa through eight key aspects. This exploration marks the beginning of an exciting series under Digital Money Movers, where we aim to uncover every facet of inclusion, ensuring no stone is left unturned.

We invite you to join us on this enlightening journey with Digital Money Movers, where each month brings discoveries and insights, contributing significantly to the discourse on digital financial inclusion in Africa.

Savings and Credit groups are common across Africa. While they have contributed greatly to the development of local communities, their strong reliance on manual and cash-based processes makes them prone to fraud and mismanagement.

But, innovators are now using technology to counter these challenges by developing platforms that digitize these savings and credit groups. One such platform in Tanzania is the Koba APP.

Koba simplifies the management of group finances, enhances communication among group members, and provides a platform for financial empowerment. It’s a versatile tool designed to facilitate collaborative financial activities and promote responsible financial practices within communities.

According to Emmanuel Zakayo, the Founder of Koba, the application eases the work of people in saving groups as they can manage their group finances digitally with every member able to apply for credit and have it approved by the leaders electronically after which it is wired by the treasurer to the borrower’s mobile money number.

“Koba is available on both the Play Store and Apple Store. You just need to download the APP and register with your mobile number. We shall then send you a confirmation code to confirm your membership. You can also create a digital savings group on Koba. You simply go to the settings, select contacts of people you want to be in the savings group, create the group name and save it.”

Zakayo noted that their biggest challenge is limited funds to scale their services and reach more people.

“We created this APP using our own personal funds. This has limited us as we can’t serve as many people as we could want because this would require more investment. We are sure that our platform is required by many groups but we cannot reach them. Hopefully, with our participation in this year’s 40 Days 40 FinTechs initiative, we shall be able to reach more people, get more customers and attract partners and investors.”

Include EveryOne Program.

We interacted with Koba on Day 40 of the 40 Days 40 FinTechs initiative for Tanzania. First implemented in Uganda, 40 Days 40 FinTechs is an annual FinTech Innovation initiative presented by HiPipo to recognize and celebrate individuals and organizations who are making significant strides in promoting financial inclusivity through the use of technology.

It is aimed at promoting innovation and collaboration among FinTechs in Africa. The initiative is designed to provide FinTechs and startups with mentorship, training, exposure, and networking opportunities to help them grow and scale their businesses.

40 Days 40 FinTechs initiative Tanzania is part of HiPipo’s broader Include EveryOne Program that is generously supported by the Gates Foundation and implemented in partnership with Level One Project, ICTC Tanzania, Ideation Corner, Cyber PLC Academy, INFITX, Crosslake Technologies, NG Films, Founders Academy and Mojaloop Foundation.

The Include EveryOne program is a beacon of acceleration of FinTech Innovation, empowerment for Women in FinTech and a catalyst for investment and development in the ICT sector. Minus 40 Days 40 FinTechs, other initiatives under the Include EveryOne Program are the FinTech Landscape Exhibition, Women in FinTech Hackathon, Summit and Incubator, Digital Impact Awards Africa and the Digital and Financial Inclusion Summit.

HiPipo is recognized as a premier advocate of digital Innovation and financial inclusion champion, a fervent proponent of the #LevelOneProject. HiPipo has been at the forefront, actively promoting digital innovation, Instant, Inclusive Payment Systems (IIPS), and DFS across Africa. With a legacy of advising, mobilizing, and facilitating the adoption of inclusive financial services, HiPipo’s efforts have been nothing short of transformative! For almost two decades, HiPipo has successfully facilitated the inclusive adoption of these crucial services.

Now and then, people have emergencies and thus seek credit services. Ideally, loans should be affordable with reasonable payment terms.

But in the real market environment, most loans are very expensive; the interests are exorbitant, and the terms unrealistic. Money Lenders, mainly loan sharks exploit borrowers who usually don’t have any alternative.

To address these challenges, BlueTick Technologies developed Mikopo Nafuu; a digital platform aimed at democratizing loans through equipping borrowers with all the necessary information about credit service providers so that they can make informed choices.

On Day 39 of the 40 Days 40 FinTechs initiative for Tanzania, we caught up with Nicholaus Ngolongolo, the Co-founder of BlueTick Technologies.

Here is the Mikopo Nafuu story as told by Nicholaus Ngolongolo.

HiPipo: What is your Financial Inclusion solution?

Nicholaus Ngolongolo: As BlueTick Technologies, we came up with a solution called Mikopo Nafuu which is a platform that regulates loan provision and gives leads to financial institutions. We have noticed that customers struggle when it comes to selecting the best financial product. When I say financial products I mean loans, credit, savings and some of insurances. They struggle to find the best products to use from what is on the market.

And sometimes they choose a product just based on what is available or because they have been referred by their friends and partners. Some of the credit products have a lot of hidden fees and high interest. Some are not even well-regulated.

When the loan officers visit them, they just accept these harsh conditions. For example, a loan officer will say we shall give you a loan of 500K but you will be 100K in interest, which is very high. So, borrowers end up paying a lot of charges and interest. These very expensive and unfair loans are very common in Tanzania.

It is from this background that we have come up with a solution which will help in regulating these lenders. We are chasing our license from the Bank of Tanzania (BOT) after which we shall register all financial providers on our platform and then assign each with a special code which every customer can refer to and check eligibility.

HiPipo: What market problem are you solving?

Nicholaus Ngolongolo: The problem that we are trying to solve is first transparency. Because customers are never given all the information they need before taking these loan products. We want to change this by ensuring that the customer gets all the required information before taking the loan. We are connecting multiple service providers so we give you all the available options and the benefits that each comes with. We give you a comparison from which you can choose what is suitable for you.

HiPipo: How does Mikopo Nafuu work?

Nicholaus Ngolongolo: We have built our platform based on two interfaces. A web application from which you can find all the services we offer. For example, we help you calculate everything about your loan; credit score, including loan fees, interest, repayment period, repayment amount and everything to expect. With this information, you can then apply and get a loan from several financial institutions. The second interface is a WhatsApp web chatbot. So, we built a boat which can interact with you and give you the same information as our website platform. You initiate the conversation with our webchat and from there, you will chat with our platform and it give you all the information regarding the loan you wish to get.

HiPipo: What is the state of FinTech Regulation in Tanzania?

Nicholaus Ngolongolo: FinTech regulations are there but I think some aspects have been missed. This has then created room for people to mistreat customers because they know they are ignorant about fees, interest and their rights. So, the regulation is there, but there are some missing parts. We as FinTechs believe we should partner with the regulators to ensure that all products are regulated and the regulation protects both the customers and innovators.

HiPipo: How does the 40 Days 40 FinTechs initiative support your cause?

Nicholaus Ngolongolo: After these kinds of stories get out there, people start to that FinTechs are solving real problems. They see the role that innovators are playing and what needs to improve. 40 Days 40 FinTechs is a huge platform and I am quite sure that these engagements and episodes that are broadcasted will reach different stakeholders. We are not only building for Africa and thus this initiative helps us reach the wider African market. We also get to know the kind of products and solutions we are competing with.

Include EveryOne Program.

First implemented in Uganda, 40 Days 40 FinTechs is an annual FinTech Innovation initiative presented by HiPipo to recognize and celebrate individuals and organizations who are making significant strides in promoting financial inclusivity through the use of technology.

It is aimed at promoting innovation and collaboration among FinTechs in Africa. The initiative is designed to provide FinTechs and startups with mentorship, training, exposure, and networking opportunities to help them grow and scale their businesses.

40 Days 40 FinTechs initiative Tanzania is part of HiPipo’s broader Include EveryOne Program that is generously supported by the Gates Foundation and implemented in partnership with Level One Project, ICTC Tanzania, Ideation Corner, Cyber PLC Academy, INFITX, Crosslake Technologies, NG Films, Founders Academy and Mojaloop Foundation.

The Include EveryOne program is a beacon of acceleration of FinTech Innovation, empowerment for Women in FinTech and a catalyst for investment and development in the ICT sector. Minus 40 Days 40 FinTechs, other initiatives under the Include EveryOne Program are the FinTech Landscape Exhibition, Women in FinTech Hackathon, Summit and Incubator, Digital Impact Awards Africa and the Digital and Financial Inclusion Summit.

HiPipo is recognized as a premier advocate of digital Innovation and financial inclusion champion, a fervent proponent of the #LevelOneProject. HiPipo has been at the forefront, actively promoting digital innovation, Instant, Inclusive Payment Systems (IIPS), and DFS across Africa. With a legacy of advising, mobilizing, and facilitating the adoption of inclusive financial services, HiPipo’s efforts have been nothing short of transformative! For almost two decades, HiPipo has successfully facilitated the inclusive adoption of these crucial services.

Japheth and Benaiah, both seasoned freelancers, had firsthand experience with the challenges of managing payments and records. Even though they would execute their work professionally and diligently, their payments and record-keeping were a mess.

‘Frustrated by the limitations of existing payment solutions, they set out on a mission to create something truly remarkable.’ They created Payd; a digitized platform aimed at addressing specific payment needs of freelancers, creatives, small businesses and entrepreneurs.

On Day 38 of the 40 Days 40 FinTechs initiative for Tanzania, we had a detailed chat with Japheth Achimba, the Director of Chaos at Payd.

We now bring you the Payd story as told by Japheth Achimba.

HiPipo: For those hearing it for the first time, what is Payd? Why should the market be interested?

Japheth Achimba: Paid is a financial management platform for freelancers and creatives across Africa. We enable them to receive their funds and manage them. This works by providing them with a platform where they can create custom no-code payment pages, and automate invoices and receipts, and they are also provided with AI-powered analytics on how to manage their finances. They can also generate payment links and QR codes.

HiPipo: How does Payd work?

Japheth Achimba: Payd users enjoy all that the platform offers through very simple steps. When one comes on the platform, s/he is prompted to create a Payd wallet. After creating this Payd wallet, you are given a unique username. With the unique username, you will be provided a payment link and now you will find all the other features available on the wallet.

HiPipo: What market problem does Payd solve?

Japheth Achimba: We are solving the problem of freelancers finding it hard to manage their finances by making it easier for them to know how much they have earned and fully account for that money. At Payd, we usually say that we are trying to make the money that Freelancers earn work for them. So, through that process of providing them with data and advising them on what they earned or made, we are making it easy for them to manage their finances.

Available statistics show that there are over 86 million Freelancers across Africa. So, if we can empower a huge number of those guys to be able to know how to manage their finances and how to spend it, it will have a great impact on them and the entire continent. You can imagine if we are able now to enable them, to get paid and receive their money instantly, it will be of great impact to them. The worry of delayed or no payments will not be there.

I don’t want to go into mentioning names, but most of the platforms available for Freelancers are chaotic and that is what we came to solve.

HiPipo: How has the market received you? Any challenges?

Japheth Achimba: With the rollout of our first version, which is now three months old, we have received good traction. We already have 1464 active users from our waitlist of freelancers we had. So, I can say so far so good. The adoption is kind of easy maybe where I can see challenges is around regulation. We are already in Kenya and Tanzania but aim to expand to more markets.

HiPipo: Your views about 40 Days 40 FinTechs.

Japheth Achimba: The 40 Days 40 FinTechs platform is an enabler for the innovators because it gives innovators exposure and a chance to shine through sharing their work. It also brings technology stakeholders together to discuss matters affecting the industry and learn from one another. This platform gives us insights to grow.

Include EveryOne Program.

First implemented in Uganda, 40 Days 40 FinTechs is an annual FinTech Innovation initiative presented by HiPipo to recognize and celebrate individuals and organizations who are making significant strides in promoting financial inclusivity through the use of technology.

It is aimed at promoting innovation and collaboration among FinTechs in Africa. The initiative is designed to provide FinTechs and startups with mentorship, training, exposure, and networking opportunities to help them grow and scale their businesses.

40 Days 40 FinTechs initiative Tanzania is part of HiPipo’s broader Include EveryOne Program that is generously supported by the Gates Foundation and implemented in partnership with Level One Project, ICTC Tanzania, Ideation Corner, Cyber PLC Academy, INFITX, Crosslake Technologies, NG Films, Founders Academy and Mojaloop Foundation.

The Include EveryOne program is a beacon of acceleration of FinTech Innovation, empowerment for Women in FinTech and a catalyst for investment and development in the ICT sector. Minus 40 Days 40 FinTechs, other initiatives under the Include EveryOne Program are the FinTech Landscape Exhibition, Women in FinTech Hackathon, Summit and Incubator, Digital Impact Awards Africa and the Digital and Financial Inclusion Summit.

HiPipo is recognized as a premier advocate of digital Innovation and financial inclusion champion, a fervent proponent of the #LevelOneProject. HiPipo has been at the forefront, actively promoting digital innovation, Instant, Inclusive Payment Systems (IIPS), and DFS across Africa. With a legacy of advising, mobilizing, and facilitating the adoption of inclusive financial services, HiPipo’s efforts have been nothing short of transformative! For almost two decades, HiPipo has successfully facilitated the inclusive adoption of these crucial services.